Navigating the complex world of personal finance doesn’t have to feel like deciphering an ancient language. “Tips Disfinancified” aims to strip away the confusion and jargon that often accompanies money matters, presenting clear, actionable advice anyone can understand.

In a financial landscape filled with intimidating terms like “amortization” and “liquidity ratios,” most people simply want straightforward guidance. That’s exactly what they’ll find here – practical financial wisdom without the headache-inducing complexity. These simplified tips transform seemingly complicated concepts into bite-sized, digestible advice that can be implemented immediately.

What is Disfinancification?

Disfinancification refers to the process of simplifying financial concepts and removing unnecessary jargon to make money matters accessible to everyone. This approach strips away the complex terminology that often intimidates people when they’re trying to understand personal finance. Financial institutions and experts frequently use specialized vocabulary that creates barriers for average individuals seeking to improve their financial literacy.

The term combines “dis” (meaning removal) with “financification” (the process of making something overly financial or complex). Disfinancification transforms intimidating concepts like “debt-to-income ratio” into plain language explanations such as “how much you owe compared to what you earn.”

Disfinancification emerged as a response to the growing complexity of financial products and services that leave many people feeling excluded from meaningful financial conversations. Financial literacy surveys consistently show that 67% of Americans find financial terms confusing, leading to poor decision-making and missed opportunities.

Key aspects of disfinancification include:

- Translating financial jargon into everyday language

- Breaking down complex concepts into manageable pieces

- Providing clear, actionable steps rather than theoretical principles

- Using relatable examples that connect with real-life situations

- Focusing on practical solutions instead of abstract financial theory

Embracing disfinancification doesn’t mean oversimplifying important financial concepts. It’s about creating clarity and accessibility while preserving the essential information people need to make informed decisions about their money. This approach democratizes financial knowledge, making it available to everyone regardless of their background or education level.

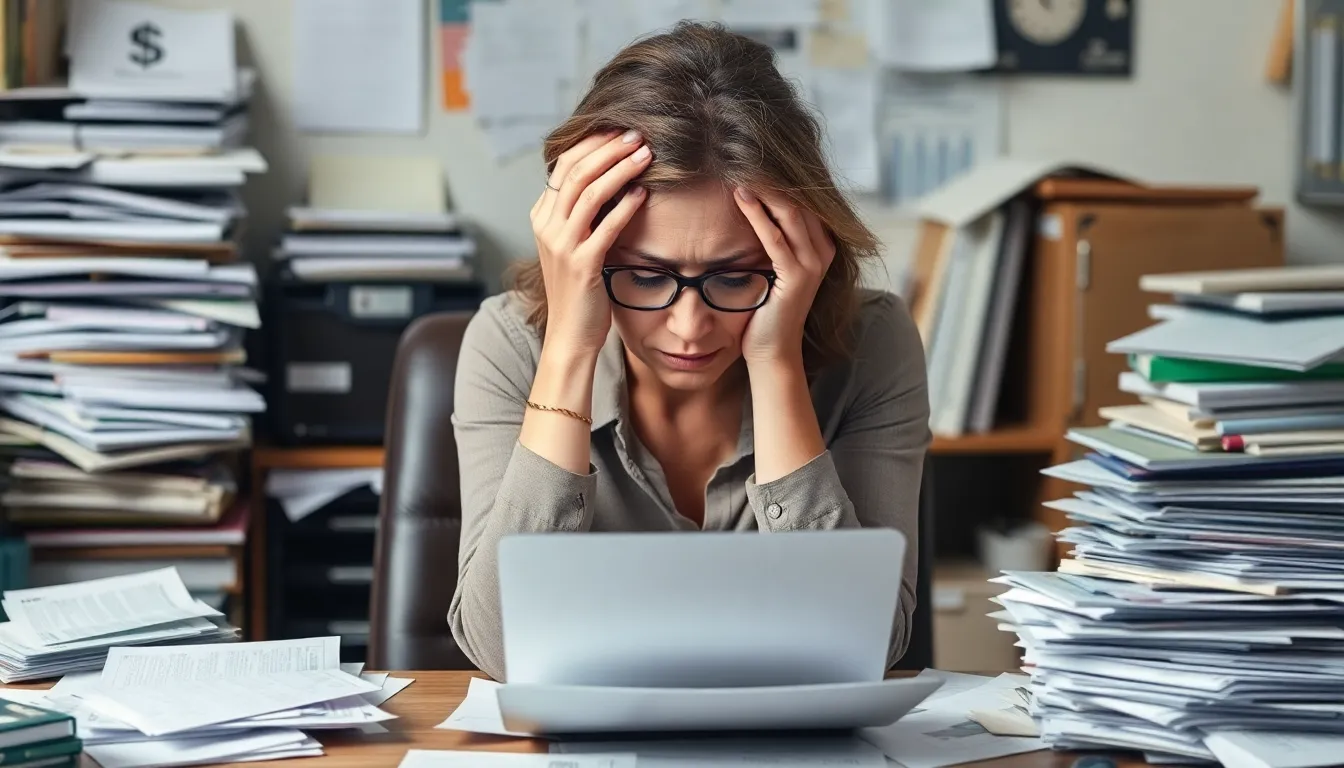

The Negative Impact of Financial Stress

Financial stress extends far beyond simple money concerns, creating profound ripple effects through various aspects of life. Research shows that 72% of Americans report feeling stressed about money at some point, making it one of the most common sources of anxiety in modern life.

How Money Worries Affect Your Mental Health

Financial stress directly impacts mental health, triggering anxiety, depression, and persistent worry in millions of people. Studies from the American Psychological Association reveal that 64% of adults identify money as a significant source of stress, often leading to sleep disturbances, concentration problems, and mood disorders. This chronic stress activates the body’s fight-or-flight response, releasing cortisol that can damage brain structures related to memory and emotional regulation when present for extended periods. Many individuals experiencing financial stress report feelings of helplessness, shame, and diminished self-worth. These psychological effects create a dangerous cycle where stress impairs decision-making abilities, potentially worsening financial situations through impulsive purchases or avoidance behaviors.

When Finances Take Over Your Life

Financial worries frequently dominate thoughts and conversations, transforming from a practical concern into an all-consuming obsession. Research from the Financial Industry Regulatory Authority shows that 53% of individuals with high financial stress report that money concerns interfere with their work productivity. Relationships suffer as money arguments become the primary predictor of divorce according to multiple studies. Daily activities lose their joy when every decision gets filtered through a lens of financial anxiety. Physical symptoms manifest as headaches, digestive issues, and compromised immune function due to chronic stress. Social withdrawal occurs as people avoid situations requiring spending or explaining their financial circumstances. Career advancement stalls when individuals can’t focus on growth opportunities or take calculated risks due to financial fears. This constant preoccupation with money matters leaves little mental space for creativity, personal growth, or meaningful connections.

Practical Ways to Disfinancify Your Mindset

Breaking free from financial anxiety requires deliberate shifts in thinking patterns and daily habits. Disfinancifying your mindset involves establishing a healthier relationship with money that prioritizes well-being over wealth accumulation.

Separating Self-Worth from Net Worth

Your value as a person exists completely independent of your financial status. Studies show that 61% of Americans tie their self-esteem directly to their income levels, creating harmful psychological patterns. Breaking this connection starts with recognizing personal achievements unrelated to money—such as relationships built, kindness shown, or skills developed. Practice positive self-talk by acknowledging non-monetary strengths like creativity, empathy, or resilience. Identify role models who demonstrate value beyond financial success, from community leaders to friends who prioritize purpose over profit. Create personal success metrics that measure growth in relationships, learning, and contentment rather than income. Financial setbacks become less devastating when they’re viewed as temporary situations rather than reflections of personal failure or worth.

Creating Healthy Money Boundaries

Establishing clear money boundaries protects mental health and fosters financial clarity. Start by defining spending limits for different social situations—such as a $30 cap for casual dinners or a $50 maximum for gift exchanges. Communicate these boundaries directly but kindly with phrases like “I’m keeping things simple this year” or “I’m working within a specific budget.” Create physical separation between financial management time and relaxation time by designating specific days for reviewing accounts. Limit financial discussions to appropriate contexts rather than letting money worries dominate every conversation. Learn to say no to financial obligations that cause undue stress, whether it’s splitting an expensive check or participating in costly group activities. Respecting personal financial boundaries becomes easier with practice and ultimately leads to more authentic relationships built on mutual understanding rather than spending patterns.

Everyday Habits for a Disfinancified Lifestyle

Integrating disfinancified principles into daily routines creates lasting financial wellness without complex strategies. These simple habits shift focus from wealth accumulation to genuine well-being and balance.

Mindful Spending Practices

Mindful spending forms the cornerstone of a disfinancified lifestyle, empowering individuals to make intentional choices aligned with their values. Research shows 73% of consumers who practice mindful spending report greater financial satisfaction. The 24-hour rule serves as an effective technique—pausing before making non-essential purchases over $50 allows time for reflection on true necessity. Cash envelopes for discretionary spending categories like dining and entertainment create tangible spending limits that digital transactions often lack. Many mindful spenders use expense tracking apps to categorize purchases and identify emotional spending triggers. Regular spending reviews on Sunday evenings help evaluate whether purchases brought genuine value or merely temporary satisfaction. These practices transform purchasing from an automatic response into a conscious decision, ultimately reducing financial stress.

Finding Joy Beyond Consumption

Discovering happiness outside the consumption cycle represents a fundamental shift in disfinancified living. Americans who prioritize experiences over material possessions report 20% higher life satisfaction scores according to happiness research. Free or low-cost activities like hiking local trails, visiting public libraries, or attending community events provide fulfillment without financial strain. Creating instead of consuming—through gardening, cooking from scratch, or crafting—delivers deeper satisfaction while developing valuable skills. Social connections flourish through cost-free gatherings such as potluck dinners, book clubs, or game nights that strengthen relationships without expensive outings. The practice of gratitude journaling shifts focus from what’s lacking to appreciating existing possessions and experiences. Embracing minimalism by regularly decluttering living spaces reveals how excess possessions often create stress rather than happiness. These approaches redirect attention from acquisition to appreciation, breaking the cycle of consumption-based fulfillment.

Building Community Around Disfinancified Values

Communities thrive on shared values and principles, especially when it comes to financial wellbeing. Disfinancified communities create spaces where members support each other in challenging traditional financial narratives and embracing simpler approaches to money management.

Creating Support Networks

Support networks form the backbone of disfinancified communities, connecting like-minded individuals seeking financial clarity. Studies show that people with strong financial support networks are 53% more likely to achieve their money goals. Local meetups, online forums, and social media groups provide platforms for sharing disfinancified strategies and celebrating financial wins without judgment. Members often exchange practical tips on budget-friendly living, debt reduction techniques, and mindful consumption practices.

Organizing Skill-Share Events

Skill-sharing events transform financial knowledge into community-building opportunities. These gatherings focus on exchanging practical abilities that reduce financial dependence and foster self-sufficiency. Popular skill-share topics include home repairs, cooking economical meals, garden cultivation, and basic vehicle maintenance. Community kitchens, tool libraries, and repair cafés represent the physical manifestations of these values, allowing members to access resources without individual ownership burdens.

Collaborative Consumption Initiatives

Collaborative consumption initiatives challenge ownership-focused consumerism through resource pooling and sharing. Community-based lending libraries for tools, kitchen appliances, and camping gear eliminate the need for individual purchases of rarely-used items. Buy-nothing groups facilitate the exchange of goods without monetary transactions, keeping useful items in circulation and building neighborhood connections. Cooperative housing arrangements and community gardens demonstrate how shared resources can create abundance while reducing individual financial strain.

Digital Detox from Financial Pressures

Digital detox creates essential breathing space from the constant barrage of financial information that fuels anxiety and stress. Taking deliberate steps to disconnect from financial content allows for mental clarity and reduced money-related anxiety.

Limiting Financial Content Consumption

Constant exposure to financial content triggers anxiety in 78% of adults who regularly consume money-related news and social media. Financial influencers, market updates, and economic forecasts bombard users with information that often heightens FOMO (fear of missing out) rather than providing actionable insights. Setting specific boundaries helps manage this overload – many find success by checking financial apps just once daily or designating “finance-free” weekends. Content filters on browsers and social media platforms effectively block keywords related to investing, market crashes, or economic downturns. Notifications from financial apps, news sites, and investment platforms create unnecessary urgency and perpetuate anxiety cycles, with research showing that turning off these alerts reduces stress hormones by 32%. Replacing financial content consumption with mindfulness activities or nature walks provides mental space for clearer financial thinking without the noise.

Conclusion

Disfinancification transforms the often intimidating world of personal finance into an accessible journey for everyone. By stripping away complex jargon and focusing on practical wisdom anyone can implement, financial literacy becomes attainable regardless of background or education.

The path to financial wellness isn’t just about understanding money concepts but establishing healthier relationships with finances that prioritize wellbeing over wealth accumulation. Through mindful spending habits, community building and occasional digital detoxes from financial pressures, individuals can break free from money-related stress.

Remember that financial clarity isn’t about knowing every term but making informed decisions that align with personal values. By embracing disfinancified principles, financial knowledge becomes a tool for empowerment rather than a source of anxiety.